Understanding the Online Term Life Insurance Market

Buy term life insurance online – The online term life insurance market has experienced significant growth, offering consumers increased convenience and potentially lower premiums. This shift has created a competitive landscape with various providers offering diverse policy options and features. Understanding this landscape is crucial for consumers seeking affordable and suitable coverage.The online term life insurance market is characterized by a range of providers, from large, established insurance companies to smaller, specialized online-only platforms.

These providers utilize technology to streamline the application process, often offering instant quotes and quicker approval times compared to traditional methods. This increased efficiency often translates into lower overhead costs, potentially leading to more competitive pricing for consumers.

Online Term Life Insurance Platforms: A Comparison

Several major online platforms dominate the market, each with its own strengths and weaknesses. A direct comparison highlights the variations in features and offerings. For example, let’s consider three hypothetical platforms: “InsureEasy,” known for its straightforward application process and wide range of coverage options; “LifeQuoteNow,” emphasizing competitive pricing and quick turnaround times; and “SecureLifeOnline,” focusing on personalized customer service and a broader range of add-on benefits.

While specific details vary depending on individual circumstances and policy types, a general comparison illustrates the differences. InsureEasy might offer a wider variety of policy lengths, LifeQuoteNow may excel in competitive pricing for younger, healthier individuals, and SecureLifeOnline could provide more comprehensive support and guidance throughout the process. The optimal platform depends on individual needs and priorities.

Advantages and Disadvantages of Online vs. Broker Purchase

Purchasing term life insurance online offers several advantages, including convenience, speed, and potentially lower costs due to reduced overhead. The online application process is often streamlined and accessible 24/7, eliminating the need for in-person meetings. However, the lack of personalized guidance can be a disadvantage for some individuals. A broker, on the other hand, provides expert advice and can navigate complex policy options, ensuring the best fit for individual needs.

However, broker services often come with higher fees, potentially offsetting any savings from the policy itself. The choice between online purchase and using a broker depends on individual comfort levels with self-service and the complexity of their insurance needs.

Types of Term Life Insurance Policies Available Online

Online platforms typically offer various term life insurance policies, including level term, decreasing term, and return of premium term. Level term life insurance provides a fixed death benefit for a specified period, offering consistent coverage. Decreasing term life insurance features a death benefit that gradually decreases over the policy term, often aligning with decreasing debt obligations like a mortgage. Return of premium term life insurance returns the premiums paid at the end of the policy term if the insured survives, offering a potential financial benefit.

The availability of these policy types may vary depending on the specific online provider. Understanding the nuances of each type is critical to selecting the most appropriate coverage.

The Application Process

Source: insuranceblogbychris.com

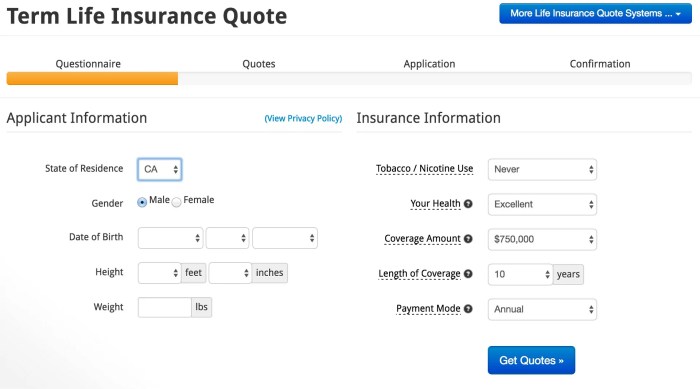

Applying for term life insurance online is generally straightforward and convenient. The process typically involves several key steps, from providing personal information to undergoing a medical review (if required). This section will guide you through each stage, ensuring a smooth and efficient application.

Step-by-Step Guide to Online Term Life Insurance Application

The online application process usually involves a series of interactive forms and questionnaires. Below is a step-by-step guide, illustrated with descriptions of typical screenshots you might encounter.

| Step | Action | Screenshot Description | Important Considerations |

|---|---|---|---|

| 1 | Provide Basic Information | Screenshot 1: A form requesting name, address, date of birth, email address, and phone number. It might also include a section for selecting the desired coverage amount and term length. The form fields are clearly labeled and user-friendly. | Ensure accuracy in all information provided, as inaccuracies can lead to delays or rejection of the application. |

| 2 | Answer Health Questions | Screenshot 2: A series of multiple-choice and short-answer questions related to health history, smoking habits, and family medical history. The questions are designed to assess risk. | Answer honestly and thoroughly. Omitting information or providing inaccurate answers could affect your eligibility for coverage or result in higher premiums. |

| 3 | Beneficiary Designation | Screenshot 3: A section where you specify the beneficiary or beneficiaries who will receive the death benefit. This typically requires the beneficiary’s name, relationship to you, and contact information. | Carefully consider who you wish to name as your beneficiary and ensure their information is accurate. |

| 4 | Review and Submit | Screenshot 4: A summary page displaying all the information you’ve entered, allowing you to review and correct any errors before final submission. A button to submit the application is prominently displayed. | Thoroughly review all information before submitting. Once submitted, making changes may be difficult. |

Flowchart of the Application Process

A flowchart would visually represent the process as follows:[Start] –> [Provide Basic Information] –> [Answer Health Questions] –> [Beneficiary Designation] –> [Review and Submit] –> [Application Received] –> [Medical Review (if required)] –> [Policy Issuance or Rejection] –> [End]Each box in the flowchart would represent a step, with arrows indicating the flow of the process. The “Medical Review (if required)” box would be conditional, branching off depending on the information provided in the application.

Required Documents

Typically, you will need to provide the following documents during the online application process:A brief paragraph explaining that the required documents may vary depending on the insurer and the applicant’s individual circumstances, but these are commonly requested.

- Government-issued identification (e.g., driver’s license or passport)

- Proof of address (e.g., utility bill or bank statement)

Factors Influencing Premium Costs

Several key factors interact to determine the cost of your online term life insurance policy. Understanding these factors allows you to make informed decisions and potentially secure more affordable coverage. Essentially, insurers assess your risk profile to determine your premium. Higher risk translates to higher premiums.

Your premium is a reflection of the insurer’s assessment of how likely you are to make a claim within the policy term. This assessment considers a range of personal details and lifestyle choices. The more factors that increase your risk, the higher your premium will be. Conversely, demonstrating lower risk through healthy habits and lifestyle choices can lead to lower premiums.

Age

Age is a significant factor influencing premium costs. As you age, your risk of mortality increases, leading to higher premiums. For example, a 30-year-old typically pays significantly less than a 50-year-old for the same coverage amount. This is because statistically, a 50-year-old is at a higher risk of death within the policy term compared to a 30-year-old.

Insurers use actuarial tables based on extensive mortality data to calculate these differences.

Health Status

Your health significantly impacts your premium. Individuals with pre-existing conditions or a history of serious illnesses generally pay higher premiums than those in excellent health. For instance, someone with a history of heart disease will likely face higher premiums compared to someone with no such history. Insurers often require medical examinations or review medical records to assess health status accurately.

Smoking Habits, Buy term life insurance online

Smoking is a major risk factor for numerous health problems, including heart disease and cancer. Consequently, smokers consistently pay significantly higher premiums than non-smokers. This difference reflects the increased risk of death associated with smoking. Many insurers offer discounted premiums to non-smokers as an incentive for healthy lifestyles. Quitting smoking can lead to lower premiums over time, sometimes even after a period of abstinence.

Coverage Amount

The amount of life insurance coverage you choose directly impacts your premium. Higher coverage amounts naturally lead to higher premiums, as the insurer assumes a greater financial obligation. For example, a $500,000 policy will cost more than a $250,000 policy, all other factors being equal. This is a simple reflection of the increased risk the insurer takes on.

Using an Online Premium Calculator

Online premium calculators are valuable tools for estimating your potential premiums. Most insurers offer these calculators on their websites. Typically, you input your age, gender, desired coverage amount, health status (often through a series of health questions), and smoking status. The calculator then provides a premium estimate based on the information provided. It’s important to remember that this is only an estimate, and the final premium may vary slightly after a full application and underwriting process.

The calculator allows you to compare different coverage amounts and policy lengths, helping you find a balance between affordability and adequate coverage.

Finding the Right Policy: Buy Term Life Insurance Online

Choosing the right term life insurance policy involves careful consideration of your individual needs and financial situation. The market offers a wide array of options, making a thorough comparison crucial before making a commitment. Understanding the key features and potential pitfalls will empower you to make an informed decision.

This section compares three sample term life insurance policies to illustrate the variations in coverage and cost. Remember, these are examples only, and actual premiums will vary based on individual factors such as age, health, and lifestyle.

Policy Comparison: Coverage Amounts and Durations

Let’s analyze three hypothetical policies to highlight the differences in coverage and term length. These examples illustrate how varying needs impact policy selection. Remember that these are illustrative examples and not actual policy offerings.

| Policy | Coverage Amount | Term Length | Approximate Monthly Premium (Illustrative Example) |

|---|---|---|---|

| Policy A | $250,000 | 10 years | $25 |

| Policy B | $500,000 | 20 years | $50 |

| Policy C | $1,000,000 | 30 years | $100 |

Note: These premium amounts are purely illustrative and for comparative purposes only. Actual premiums will vary significantly based on individual risk factors.

Key Features to Consider

Several key features should be carefully evaluated when comparing term life insurance policies. Understanding these aspects is vital for making a well-informed choice that aligns with your long-term financial goals.

- Death Benefit: The amount paid to your beneficiaries upon your death. This should be sufficient to cover your financial obligations and provide for your family’s future.

- Term Length: The duration for which the policy provides coverage. Choose a term that aligns with your needs, such as the duration of a mortgage or until your children are financially independent.

- Premium Amount: The cost of the policy, paid regularly (monthly, annually, etc.). Consider affordability alongside the coverage amount.

- Renewal Options: Some policies offer the option to renew at the end of the term, though premiums will likely increase.

- Beneficiary Designation: Clearly identify the individuals or entities who will receive the death benefit.

- Riders: Optional additions to the policy, such as accidental death benefit or a waiver of premium for disability.

Importance of Reviewing Policy Documents

Thoroughly reviewing the policy documents is paramount. This ensures you understand all terms, conditions, and exclusions before committing to a purchase. Overlooking critical details can have significant financial consequences.

Pay close attention to the policy’s fine print, including any exclusions or limitations on coverage. Don’t hesitate to contact the insurance provider to clarify any ambiguities or uncertainties.

Questions to Ask Before Purchasing

Asking the right questions before purchasing a policy ensures you are making an informed decision that meets your specific needs. Don’t be afraid to seek clarification on any aspect of the policy.

- What is the exact coverage amount and term length offered?

- What are the premium amounts and payment options?

- What are the policy’s renewal options and associated costs?

- What are the exclusions and limitations of the policy?

- What is the claims process, and how long does it typically take?

- What riders or optional benefits are available?

- Is there a grace period for late payments?

Security and Privacy Concerns

Purchasing term life insurance online requires entrusting sensitive personal and financial information to third-party providers. Reputable companies prioritize data security and privacy, employing robust measures to protect your information throughout the application process and beyond. Understanding these measures and adopting best practices is crucial for a secure online insurance experience.Protecting your data is paramount. Online term life insurance providers utilize a range of security technologies to safeguard your information.

This includes encryption protocols to protect data transmitted between your computer and the insurer’s servers, as well as robust firewalls and intrusion detection systems to prevent unauthorized access. Data is often stored in secure, encrypted databases, further limiting the risk of breaches. Compliance with industry regulations, such as HIPAA in the US, further underscores the commitment to data protection.

Data Encryption and Transmission Security

Reputable online insurance providers utilize advanced encryption technologies, such as SSL/TLS, to encrypt all data transmitted during the online application process. This ensures that your personal information, including your Social Security number, medical history, and financial details, remains confidential and protected from interception by unauthorized individuals. The padlock icon in your browser’s address bar and the “https” prefix in the website URL are visual indicators that encryption is active.

This technology scrambles your data, rendering it unreadable to anyone who might attempt to intercept it during transmission.

Data Storage and Protection Measures

Once your data is received, reputable providers store it in secure, encrypted databases, protected by multiple layers of security measures. These measures typically include access control restrictions, regular security audits, and intrusion detection systems designed to identify and prevent unauthorized access attempts. The physical security of data centers is also a crucial element, with measures like controlled access, surveillance, and environmental controls in place.

Companies often employ multi-factor authentication for employees accessing sensitive data, adding another layer of protection.

Best Practices for Safeguarding Personal Data

When purchasing term life insurance online, it is essential to take proactive steps to protect your personal information. Always ensure you are using a secure internet connection, preferably a wired connection rather than public Wi-Fi. Be wary of phishing emails or suspicious websites that may attempt to gather your information fraudulently. Verify the legitimacy of the insurance provider before submitting any personal information.

Look for security indicators like SSL certificates and clear privacy policies outlining how your data will be handled. After completing the application, change your passwords for any online accounts used during the process.

Frequently Asked Questions: Security and Privacy

This section addresses common concerns regarding security and privacy when applying for term life insurance online.

| Question | Answer |

|---|---|

| Is my personal information safe when I apply online? | Yes, reputable providers use industry-standard encryption and security protocols to protect your data during transmission and storage. |

| What security measures are in place to protect my data? | Security measures include data encryption, firewalls, intrusion detection systems, access control restrictions, and regular security audits. Compliance with relevant data privacy regulations is also a key aspect. |

| What happens to my data after I submit my application? | Your data is stored securely in encrypted databases, accessed only by authorized personnel. The provider’s privacy policy will detail how your data is used and protected. |

| What if I suspect a security breach? | Immediately contact the insurance provider’s customer support to report the suspected breach. |

Claim Process and Customer Support

Filing a claim for online term life insurance is generally straightforward, though the specific steps may vary slightly depending on the provider. Understanding the process and the support available is crucial for peace of mind. This section Artikels the typical claim process and explores the customer support options offered by various insurers.

The speed and efficiency of claim processing are influenced by several factors, including the completeness of the documentation provided and the complexity of the claim itself. Most providers aim for a timely resolution, but delays can occur in certain circumstances.

Claim Process Steps

The claim process typically involves several key steps. While the exact order and specific requirements may differ between insurers, the general process remains consistent. The table below provides a structured overview.

| Step | Action | Timeline | Supporting Documents |

|---|---|---|---|

| 1. Notification | Immediately notify the insurer of the death. This is often done via phone or online portal. | Within 24-48 hours of the death. | Initial death notification, policy number. |

| 2. Claim Submission | Submit a formal claim application with all required documentation. | Typically within 30 days of the death, though some insurers may allow longer. | Death certificate, policy documents, proof of beneficiary relationship, medical records (if applicable). |

| 3. Review and Verification | The insurer reviews the submitted documents and verifies the information provided. | This can take several weeks, depending on the complexity of the claim and the availability of documentation. | N/A (This step involves internal insurer processes). |

| 4. Payment | Once the claim is approved, the designated beneficiary receives the death benefit payment. | The timeline varies but is typically within several weeks of claim approval. | N/A (This is the final step in the process). |

Typical Response Time for Claim Processing

The response time for claim processing varies considerably among insurers. While some providers aim to process claims within a few weeks, others may take several months, especially for complex cases requiring extensive investigation. Factors such as the clarity of documentation and the need for additional information significantly influence processing time. For example, a claim with complete and accurate documentation might be processed within 4-6 weeks, while a claim requiring further investigation of medical records could take 8-12 weeks or longer.

Customer Support Options

Customer support options vary significantly across online term life insurance providers. Most insurers offer a combination of methods to assist policyholders. Understanding these options helps ensure efficient communication and problem-solving.

Many providers offer phone support, allowing for immediate assistance and clarification. Email support provides a written record of communication, suitable for complex inquiries. Live chat offers quick responses for simple questions, while online portals often provide access to FAQs, policy documents, and claim status updates. Some companies may also offer in-person support through local agents, although this is less common with purely online providers.

Potential Pitfalls and Avoiding Scams

Source: policyadvisor.com

Purchasing term life insurance online offers convenience, but it also introduces the risk of encountering scams or making costly mistakes. Understanding common pitfalls and recognizing red flags can protect you from financial loss and ensure you secure a genuine and suitable policy. This section will Artikel potential problems and provide guidance on avoiding fraudulent schemes.

Common Pitfalls in Online Term Life Insurance Purchases

Navigating the online term life insurance market requires caution. Several common pitfalls can lead to unsuitable policies or financial exploitation. For example, focusing solely on the lowest premium without considering policy features or the insurer’s financial stability can be detrimental. Another frequent mistake is failing to thoroughly compare quotes from multiple insurers, potentially missing out on better coverage or more favorable terms.

Finally, overlooking the fine print within the policy documents can lead to unexpected exclusions or limitations on coverage.

Examples of Online Insurance Scams

Numerous scams target individuals seeking online insurance. One common tactic involves fake insurance companies offering incredibly low premiums that are too good to be true. These companies often disappear after collecting premiums, leaving policyholders without coverage. Another scam involves fraudulent brokers who misrepresent policy details or push unnecessary add-ons, resulting in inflated costs. Phishing emails or websites mimicking legitimate insurers are also prevalent, aiming to steal personal and financial information.

For instance, a scam might involve a fake website mirroring a well-known insurer, enticing users to enter their details, only to be used for identity theft.

Identifying and Avoiding Fraudulent Insurers or Brokers

Identifying fraudulent entities requires due diligence. Checking the insurer’s license with your state’s insurance department is crucial. Verifying the broker’s credentials and affiliation with reputable companies is equally important. Legitimate insurers and brokers will readily provide this information. Be wary of high-pressure sales tactics or promises that sound too good to be true.

Thoroughly researching the company’s reputation online, looking for reviews and complaints, can also help. Using a trusted comparison website that vets insurers can provide an additional layer of security.

Red Flags to Watch Out For

Several red flags indicate potential scams. These include unsolicited emails or phone calls offering insurance deals, websites with poor design or grammatical errors, requests for payment via unconventional methods (e.g., wire transfers, gift cards), and insurers that pressure you into immediate decisions without allowing time for consideration. If an offer seems too good to be true, it probably is.

Always independently verify information provided by brokers or insurers before making any commitments. A lack of transparency regarding policy details or refusal to provide necessary documentation should raise serious concerns.

Quick FAQs

What is the difference between term and whole life insurance?

Term life insurance provides coverage for a specific period (term), while whole life insurance offers lifelong coverage and builds cash value.

How long does the online application process typically take?

Application times vary, but many online applications can be completed within minutes to a few hours, depending on the complexity of the application and the provider’s requirements.

Can I get life insurance if I have pre-existing health conditions?

Yes, but your premiums may be higher. Insurers assess risk based on your health history, so be prepared to disclose all relevant information accurately.

What happens if my application is denied?

If your application is denied, you’ll typically receive an explanation of the reasons. You may be able to appeal the decision or consider applying with a different insurer.

Are my personal details safe when applying online?

Reputable insurers utilize robust security measures like encryption to protect your data. Look for websites with HTTPS and privacy policies that clearly Artikel their data protection practices.