Understanding the Search Intent Behind “Get Multiple Car Insurance Quotes”

Source: googleusercontent.com

The search query “Get multiple car insurance quotes” reveals a user actively engaged in the car insurance shopping process. It signifies a proactive approach to finding the best possible coverage at the most competitive price, indicating a desire for comparison and informed decision-making. This contrasts with a passive approach, such as simply searching for “car insurance,” which suggests a more preliminary stage of research.The motivations behind this search are multifaceted and reflect various stages of the car insurance buying journey.

Users are not simply looking for any quote; they are specifically seeking out multiple options to compare. This suggests a higher level of engagement and a greater emphasis on value.

User Needs and Goals

Users searching for multiple car insurance quotes have a range of needs and goals. Some might be renewing their existing policy and seeking better rates. Others might be purchasing insurance for a new car, while some might be switching providers due to dissatisfaction with their current insurer. Regardless of the specific circumstance, the underlying goal is consistent: to secure the most suitable car insurance policy at an affordable price.

For example, a new driver might prioritize finding affordable coverage with minimal restrictions, while an experienced driver with a clean record might focus on finding the lowest premium for comprehensive coverage. A user purchasing a high-value vehicle might prioritize extensive coverage options, even if it means a higher premium.

Stages of the Car Insurance Buying Process

The search query “Get multiple car insurance quotes” typically reflects a user who has progressed beyond the initial research phase. They’ve likely already established a basic understanding of car insurance types and coverage options. This search query directly points to the comparison and selection stages of the buying process. The user is actively seeking out specific information to make a comparison between different providers and policies, which means they are closer to making a purchase decision.

This is a critical stage where the user weighs factors such as price, coverage, and provider reputation before committing to a policy.

User Urgency and Knowledge

The level of urgency and knowledge varies among users employing this search query. Some might be facing an imminent deadline, such as needing insurance before a specific date (e.g., a new car purchase). Others might have more flexibility in their timeline. In terms of knowledge, while the user demonstrates a certain level of understanding by seeking multiple quotes, their knowledge might still be limited.

They may require further clarification on specific policy details or coverage options after receiving their quotes. A user renewing their policy will likely possess a greater degree of familiarity with the process and the terminology than a first-time buyer. For example, a user purchasing their first car might be less familiar with concepts such as liability limits and deductibles, while a seasoned driver might focus on specific policy features like roadside assistance or accident forgiveness.

Methods for Obtaining Multiple Car Insurance Quotes: Get Multiple Car Insurance Quotes

Source: medium.com

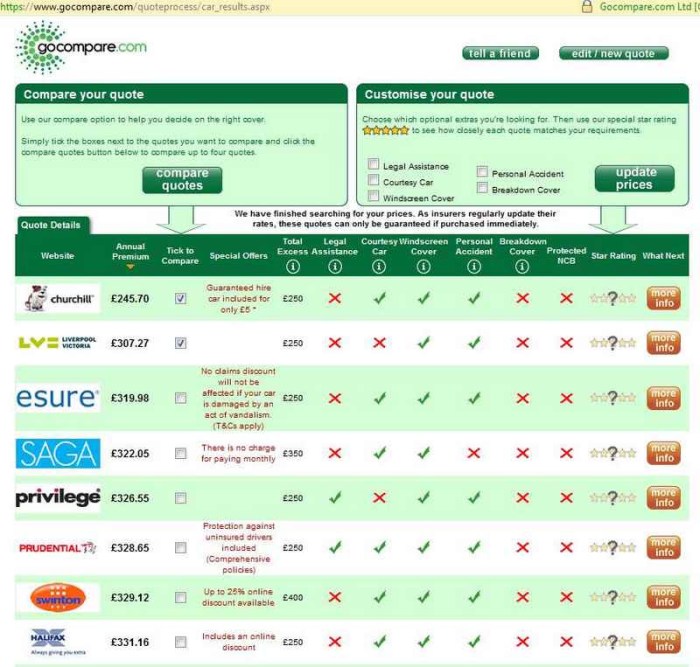

Securing the best car insurance rates requires comparing quotes from multiple providers. This ensures you find a policy that meets your needs and budget without compromising coverage. Several methods exist to efficiently gather these quotes, each with its own advantages and disadvantages.

Obtaining multiple car insurance quotes involves leveraging various platforms and resources. Understanding the differences between these options will allow you to choose the most efficient and effective strategy for your situation. This comparison will focus on three primary methods: online comparison websites, individual insurer websites, and insurance brokers.

Comparison of Quote Acquisition Methods

Online quote comparison websites, individual insurer websites, and insurance brokers each offer a distinct approach to obtaining car insurance quotes. The optimal choice depends on factors like your comfort level with technology, time constraints, and desired level of personalized service.

Online comparison websites aggregate quotes from multiple insurers, simplifying the process. However, they may not include every insurer in your area, and the displayed quotes might be simplified versions of the actual policies. Individual insurer websites provide direct access to specific company offerings but require visiting multiple sites. Insurance brokers offer personalized assistance, guiding you through the process and potentially accessing insurers not available through online platforms.

However, this personalized service usually comes with a higher time investment.

Step-by-Step Guide for Obtaining Three Quotes

To secure competitive car insurance rates, obtaining quotes from at least three different providers is recommended. The following steps Artikel a straightforward process, regardless of the chosen method.

| Provider | Quote Process | Features Offered | Estimated Price Range (Example) |

|---|---|---|---|

| Online Comparison Website (e.g., NerdWallet, The Zebra) | Enter vehicle and driver information; compare displayed quotes. | Quick comparison, multiple insurers, potential discounts highlighted. | $800 – $1500 annually |

| Individual Insurer Website (e.g., Geico, State Farm, Progressive) | Navigate to each insurer’s website; fill out individual quote forms. | Detailed policy information, direct communication with insurer. | $750 – $1600 annually |

| Insurance Broker (Local or Online) | Contact broker; provide necessary information; receive personalized recommendations. | Personalized service, access to niche insurers, potential negotiation. | $850 – $1700 annually |

Factors Influencing Quote Accuracy and Reliability

The accuracy and reliability of online car insurance quotes can be affected by several factors. Understanding these influences is crucial for making informed decisions based on the quotes received.

Several factors can impact the accuracy of online quotes. For instance, incomplete or inaccurate information provided during the quote request process will lead to inaccurate pricing. The algorithms used by comparison websites and individual insurers may also differ, resulting in variations in the quoted price. Furthermore, the quotes are often based on generalized risk assessments and may not fully reflect individual circumstances, such as specific driving history details beyond simple accidents and violations.

Finally, the availability of discounts and promotions may vary, further influencing the final price.

Factors Influencing Car Insurance Quote Prices

Several interconnected factors determine the price you pay for car insurance. Understanding these elements allows for a more informed approach to securing the best possible coverage at a competitive rate. This understanding empowers consumers to make choices that can significantly impact their premiums.Several key variables significantly influence the cost of your car insurance. These factors are often weighted differently by insurance companies, resulting in varying premiums across different individuals and situations.

Age and Driving History

Your age and driving history are two of the most significant factors affecting your car insurance premiums. Younger drivers, particularly those with less than three years of driving experience, are statistically more likely to be involved in accidents, leading to higher premiums. A clean driving record, free of accidents and traffic violations, will generally result in lower rates. Conversely, multiple accidents or traffic violations, especially those involving serious injury or property damage, can substantially increase your premiums.

For example, a young driver with a speeding ticket might see a 20-30% increase compared to a driver with a clean record of the same age. A history of at-fault accidents could lead to even higher increases.

Vehicle Type

The type of vehicle you drive plays a crucial role in determining your insurance cost. Sports cars, luxury vehicles, and high-performance models are generally more expensive to insure due to their higher repair costs and increased risk of theft. Conversely, smaller, less expensive vehicles typically command lower premiums. For instance, insuring a high-performance sports car will cost significantly more than insuring a compact sedan, even if both drivers have identical driving records.

The vehicle’s safety features, such as anti-lock brakes and airbags, also influence the premium. Vehicles with advanced safety features may qualify for discounts.

Location

Your location significantly impacts your car insurance rates. Insurance companies consider factors such as the crime rate, accident frequency, and the cost of repairs in your area. Urban areas with high traffic density and higher rates of theft tend to have higher insurance premiums than rural areas. For example, a driver living in a large city with a high crime rate might pay considerably more than a driver in a small, rural town, even if all other factors are identical.

Credit Score

In many states, your credit score is a factor in determining your car insurance premiums. Insurers often use credit-based insurance scores, which are different from your traditional FICO score, to assess your risk. A good credit score generally correlates with responsible financial behavior, which insurers often view as an indicator of lower risk. Conversely, a poor credit score may result in higher premiums.

The exact impact varies by state and insurance company, but a lower credit score can lead to a noticeable increase in premiums. This is because insurance companies consider credit scores as a predictor of future claims behavior.

Optional Coverages

Adding optional coverages, such as collision and comprehensive coverage, increases your overall premium. Collision coverage pays for damage to your vehicle in an accident, regardless of fault. Comprehensive coverage protects against damage from events other than collisions, such as theft, vandalism, or weather-related damage. While these coverages offer valuable protection, they add to the cost of your insurance. The extent of the increase depends on factors such as the value of your vehicle and the deductibles you choose.

For example, adding collision and comprehensive coverage to a policy could increase the premium by 20-40%, depending on the vehicle’s value and the selected deductibles.

Comparing and Evaluating Car Insurance Quotes

Receiving multiple car insurance quotes is only half the battle; effectively comparing and evaluating them is crucial to securing the best coverage at the most affordable price. This involves a methodical approach, ensuring you understand the details of each policy and identify the best fit for your individual needs and budget.

Side-by-Side Comparison of Car Insurance Quotes

To facilitate a clear comparison, creating a side-by-side template is highly recommended. This allows for quick visual identification of key differences between policies. Listing the essential features in a structured format enhances the comparison process significantly.

| Insurance Company | Annual Premium | Deductible (Collision) | Deductible (Comprehensive) | Liability Coverage | Uninsured/Underinsured Motorist Coverage | Comprehensive Coverage | Collision Coverage | Rental Reimbursement | Roadside Assistance | Other Coverages |

|---|---|---|---|---|---|---|---|---|---|---|

| Company A | $1200 | $500 | $250 | 100/300/100 | 100/300 | Yes | Yes | Yes | No | None |

| Company B | $1000 | $1000 | $500 | 100/300/100 | 250/500 | Yes | Yes | No | Yes | Towing |

| Company C | $1500 | $250 | $100 | 250/500/250 | 250/500 | Yes | Yes | Yes | Yes | Accident Forgiveness |

Note: Liability coverage is expressed as 100/300/100, representing $100,000 bodily injury liability per person, $300,000 bodily injury liability per accident, and $100,000 property damage liability. These figures are examples and may vary widely depending on the provider and coverage options.

Interpreting Policy Details and Coverage Limits

Understanding policy details is paramount. Coverage limits define the maximum amount the insurer will pay for a specific claim. For instance, a $100,000 bodily injury liability limit means the insurer will pay a maximum of $100,000 for injuries caused to another person in an accident. Deductibles represent the amount you pay out-of-pocket before the insurance coverage kicks in.

A higher deductible typically leads to lower premiums. Carefully review the policy documents to understand the specific coverages included, exclusions, and any limitations. Consider factors such as the age and condition of your vehicle when assessing the appropriateness of the chosen deductibles. Higher deductibles are generally more suitable for older vehicles where the repair costs may be less than the deductible itself.

Negotiating Lower Premiums

Once you’ve compared quotes, don’t hesitate to negotiate. Insurance companies are often willing to offer discounts. Highlight your clean driving record, multiple vehicle insurance, or other factors that demonstrate low risk. Inquire about potential discounts for bundling home and auto insurance, safety features in your vehicle, or completing defensive driving courses. Be prepared to switch providers if a better offer isn’t presented.

Remember to always compare the overall value – including coverage – not just the price.

Illustrating the Quote Comparison Process

Source: gajizmo.com

Let’s walk through a practical example of comparing car insurance quotes to highlight the benefits of obtaining multiple offers before making a decision. This will demonstrate how a simple comparison can lead to significant savings.Imagine Sarah, a 32-year-old with a clean driving record, owns a 2018 Honda Civic. She lives in a suburban area and commutes approximately 15 miles daily to her office job.

She’s looking for comprehensive car insurance coverage. She requests quotes from four different insurance providers: Company A, Company B, Company C, and Company D.

Car Insurance Quote Comparison

The following table summarizes the quotes Sarah received, highlighting key differences in coverage and pricing. Note that the exact prices would vary depending on location and specific coverage details. This example provides a realistic representation.

| Insurance Company | Annual Premium | Deductible (Collision) | Deductible (Comprehensive) | Coverage Details |

|---|---|---|---|---|

| Company A | $1200 | $500 | $500 | Comprehensive coverage, roadside assistance, rental car reimbursement. |

| Company B | $1050 | $1000 | $1000 | Comprehensive coverage, accident forgiveness. |

| Company C | $1350 | $250 | $250 | Comprehensive coverage, higher liability limits, accident forgiveness, 24/7 claims support. |

| Company D | $980 | $1000 | $1000 | Comprehensive coverage, but lacks roadside assistance. |

Choosing the Best Car Insurance Policy, Get multiple car insurance quotes

After reviewing the quotes, Sarah considers her priorities. While Company D offers the lowest premium, the lack of roadside assistance is a concern. Company C offers superior coverage but at a higher price. She carefully weighs the value of features like lower deductibles (Company A and C) versus the cost savings of higher deductibles (Company B and D).

Ultimately, she decides that Company B’s balance of price and coverage best suits her needs and budget.

Potential Savings from Multiple Quotes

By obtaining multiple quotes, Sarah identified a potential savings of $220 compared to the most expensive quote (Company C) and $120 compared to the first quote she might have received. This illustrates the significant financial advantage of shopping around. Had Sarah only contacted Company C, she would have paid considerably more for similar coverage. This highlights the importance of comparing before committing to a policy.

Addressing Potential Pitfalls and Misconceptions

Comparing car insurance quotes can seem straightforward, but several pitfalls can lead to an inadequate or even costly policy. Understanding these common mistakes and potential hidden issues is crucial for securing the best coverage at the most competitive price. Failing to thoroughly investigate all aspects of a policy can have significant financial repercussions.Many people make critical errors when comparing car insurance quotes, often resulting in inadequate coverage or unexpectedly high costs.

Overlooking crucial details during the comparison process can lead to substantial financial burdens down the line. A thorough understanding of policy details and potential hidden fees is paramount to securing optimal protection.

Common Mistakes in Comparing Car Insurance Quotes

Failing to accurately assess your individual needs and comparing only price, without considering coverage limits and deductibles, is a frequent error. Another common mistake is selecting the first quote received without exploring other options. Furthermore, many overlook the importance of reading the fine print and understanding policy exclusions. Finally, some individuals fail to regularly review and update their insurance policy to reflect changes in their circumstances, such as a change of address or a new car.

The Importance of Thoroughly Reading Policy Documents

Reading the policy document thoroughly is not merely a formality; it’s a critical step in ensuring you understand exactly what you’re paying for and what coverage you’re receiving. Many policies contain complex jargon and legal language that can be difficult to decipher. However, neglecting this step can result in unpleasant surprises when making a claim. For example, a seemingly comprehensive policy might exclude certain types of damage or have limitations on coverage amounts that are not immediately apparent.

Take the time to understand the terms, conditions, and exclusions to avoid future complications.

Potential Hidden Fees or Limitations Within Insurance Policies

Hidden fees and limitations are often embedded within the fine print of insurance policies. These can significantly increase the overall cost of insurance and restrict the extent of coverage. For instance, some policies may charge additional fees for optional add-ons that are not clearly advertised. Other policies might impose limitations on the amount of coverage for specific types of claims, such as accidents involving uninsured drivers or damage caused by natural disasters.

Furthermore, certain policies may have stipulations regarding the repair shops you can utilize, potentially impacting the quality of repairs and increasing out-of-pocket expenses. Understanding these hidden costs and limitations is vital to making an informed decision.

Top FAQs

What if I have a poor driving record?

Insurers will consider your driving history, including accidents and violations. Getting multiple quotes allows you to see how different companies weigh this factor. Some may be more lenient than others.

How long does the quote process usually take?

Obtaining quotes online can be very quick, often taking just minutes per insurer. Working with a broker may take slightly longer, as they’ll need to gather information and present options.

Can I get quotes without providing my personal information?

Most insurers require some personal information to generate accurate quotes, but the level of detail needed varies. Some comparison sites offer initial estimates without full details.

What happens if I find a better quote after purchasing a policy?

You can typically cancel your current policy and switch to a better offer, but be aware of potential cancellation fees. Contact your insurer to discuss options.

Are there any hidden fees I should be aware of?

Carefully review the policy documents for any administrative fees, processing fees, or other charges that are not immediately apparent in the initial quote.