Three business insurance reviews – Protecting your business is paramount. A robust insurance strategy safeguards your assets, your employees, and your future. But navigating the world of business insurance can be daunting. This comprehensive guide reviews three key types of business insurance – General Liability, Commercial Auto, and Workers’ Compensation – providing detailed information to help you make informed decisions. We’ll explore their coverage, benefits, and potential drawbacks, ensuring you’re equipped to choose the right policies for your specific needs.

1. General Liability Insurance

Protecting Your Business from Everyday Risks

General liability insurance, often called GL insurance, is a cornerstone of any comprehensive business insurance plan. It protects your business from financial losses arising from accidents, injuries, or property damage caused by your business operations or your employees. This coverage is crucial, regardless of your business size or industry.

Source: consumersadvocate.org

What Does General Liability Insurance Cover?, Three business insurance reviews

- Bodily injury liability: Covers medical expenses and legal costs if someone is injured on your business property or as a result of your business operations.

- Property damage liability: Covers the cost of repairing or replacing someone else’s property if it’s damaged due to your business activities.

- Personal and advertising injury liability: Protects against claims of libel, slander, copyright infringement, or other similar offenses.

Why is General Liability Insurance Important?

Even small businesses face the risk of lawsuits. A single accident or incident can lead to significant financial losses, potentially crippling your business. General liability insurance provides a crucial safety net, covering legal fees, settlements, and judgments, allowing you to continue operating without facing financial ruin. It also enhances your credibility and professionalism, reassuring clients and partners of your commitment to risk management.

Choosing the Right General Liability Policy

The cost of general liability insurance varies depending on factors such as your industry, business size, location, and claims history. It’s essential to work with an experienced insurance broker to determine the appropriate coverage limits and policy features for your specific needs. Consider factors like your revenue, the number of employees, and the nature of your business operations when assessing your coverage requirements.

Don’t underestimate the importance of adequate coverage; underinsurance can leave you vulnerable in the event of a significant claim.

2. Commercial Auto Insurance

Protecting Your Vehicles and Drivers

If your business uses vehicles for deliveries, transportation, or employee commuting, commercial auto insurance is a must. This type of insurance protects your business from financial losses resulting from accidents or damage involving your company vehicles. It offers broader coverage than personal auto insurance, addressing the unique risks associated with business operations.

What Does Commercial Auto Insurance Cover?

- Liability coverage: Protects you from financial responsibility if your employee causes an accident resulting in injury or property damage to others.

- Collision coverage: Covers damage to your vehicle in an accident, regardless of fault.

- Comprehensive coverage: Covers damage to your vehicle from events other than collisions, such as theft, vandalism, or natural disasters.

- Uninsured/underinsured motorist coverage: Protects you if you’re involved in an accident with an uninsured or underinsured driver.

The Importance of Commercial Auto Insurance Compliance

Operating a business vehicle without adequate insurance can result in significant fines and legal penalties. Commercial auto insurance ensures compliance with state and federal regulations, protecting your business from potential legal ramifications. Furthermore, it demonstrates responsible business practices, building trust with clients and stakeholders. Regularly reviewing your policy to ensure it adequately covers your fleet and operational needs is crucial.

3. Workers’ Compensation Insurance

Protecting Your Employees

Workers’ compensation insurance is a legally mandated insurance policy in most states, designed to protect your employees in case of work-related injuries or illnesses. It covers medical expenses, lost wages, and rehabilitation costs for employees injured on the job, regardless of fault. Failing to secure adequate workers’ compensation coverage can lead to significant legal and financial repercussions.

What Does Workers’ Compensation Insurance Cover?

- Medical expenses: Covers all reasonable and necessary medical treatment related to the work injury.

- Lost wages: Provides temporary disability benefits to replace lost income while the employee recovers.

- Rehabilitation: Covers the costs of physical therapy, vocational rehabilitation, and other services to help the employee return to work.

- Death benefits: Provides financial support to the employee’s dependents in the event of a work-related fatality.

Understanding Workers’ Compensation Claims

The claims process can be complex, involving medical evaluations, legal documentation, and ongoing communication with insurance providers. Maintaining accurate records of employee injuries and promptly reporting incidents to your insurance carrier is crucial for efficient claims processing. Understanding your responsibilities as an employer under workers’ compensation laws is essential to avoid potential disputes and ensure compliance.

Frequently Asked Questions (FAQs)

- Q: How much does business insurance cost? A: The cost varies greatly depending on factors like your industry, location, coverage limits, and claims history. It’s best to obtain quotes from multiple insurers.

- Q: What happens if I don’t have business insurance? A: Depending on your location and industry, operating without necessary insurance can lead to significant fines, lawsuits, and financial ruin in the event of an accident or incident.

- Q: How do I choose the right insurance provider? A: Compare quotes from multiple insurers, consider their reputation and customer service, and look for policies that offer the appropriate coverage limits and features for your specific needs. Working with an independent insurance broker can be beneficial.

- Q: Can I bundle my business insurance policies? A: Yes, many insurers offer discounts for bundling multiple policies, such as general liability, commercial auto, and workers’ compensation.

- Q: What are the penalties for not having workers’ compensation insurance? A: Penalties vary by state but can include significant fines, legal action, and potential business closure.

Resources

- Insureon (Insurance comparison site)

- The Hartford (Major business insurance provider)

- Small Business Insurance Types (Informative article)

Call to Action

Protecting your business is an investment in its future. Don’t wait until it’s too late. Contact an insurance broker today to review your current coverage and ensure you have the protection you need. Get a free quote and secure your business’s future!

Quick FAQs: Three Business Insurance Reviews

What types of business insurance are commonly reviewed?

Commonly reviewed types include general liability, professional liability (errors and omissions), commercial property, workers’ compensation, and business interruption insurance.

Source: topconsumerreviews.com

How do I compare business insurance quotes effectively?

Compare quotes based on coverage limits, deductibles, premiums, and the insurer’s reputation and financial stability. Don’t solely focus on price; ensure the coverage adequately protects your business.

What should I look for in a reputable insurance provider?

Look for an A-rated insurer with a strong track record, positive customer reviews, and readily available customer service. Consider their claims handling process and financial strength ratings.

Source: fbinsure.com

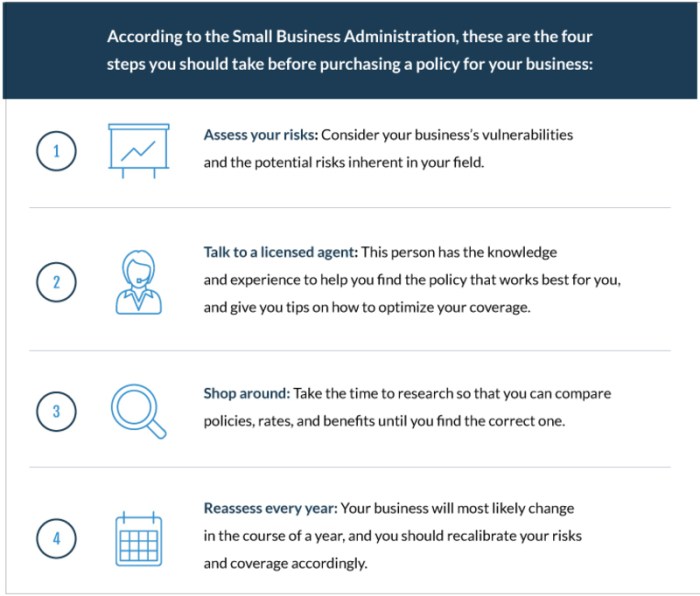

How often should I review my business insurance policy?

Review your policy annually or whenever there’s a significant change in your business operations, such as expansion, new equipment, or increased employee count.